Best Cars to Lease in 2026: High Residual Vehicles Worth Your Money

Not every car leases equally well. These are the best cars to lease in 2026 based on residual value, manufacturer incentives, and real depreciation math.

We have all been there—staring at a dealer's worksheet wondering if the cheaper monthly payment is actually a trap. Let's run the exact math so you know which option actually saves you money over the long haul.

Current Auto Market Update (2026)

Average new car loan rates are currently sitting at 6.5% - 7.5%. Lease money factors have improved slightly to an average of 0.00125 (3.0% APR). Strong residuals on mid-size SUVs make leasing highly competitive this quarter.

Explore our complete suite of auto loan, depreciation, and refinancing calculators.

Calculate your monthly car payment and total interest over the life of your auto loan.

Find out how much car you can afford based on your desired monthly payment and loan terms.

Estimate how much a vehicle's value will drop over time to make smarter buying and leasing decisions.

Calculate how much money you can save by refinancing your current auto loan to a lower interest rate.

Estimate your monthly car lease payment using MSRP, residual value, money factor, and fees.

Calculate your monthly car payment for a new or used vehicle purchase with taxes, fees, and trade-in.

Calculate the true total cost of owning a car including payments, insurance, fuel, maintenance, and depreciation.

"I was convinced leasing a Camry would be cheaper, but this calculator showed me that buying and keeping it for 5 years actually saves me $3,000 in the long run. The month-by-month breakdown is eye-opening."

Sarah J.

Bought a 2025 Toyota Camry

"The Deal Score feature is incredible. I plugged in the dealer's lease quote and it got a D. I negotiated the money factor down to the base rate and got it to an A-. Saved me $45 a month instantly."

Mike T.

Leased a Honda CR-V

"No other calculator accounts for Texas taxes being charged upfront on the full price of the car! This tool helped me realize that leasing in Texas is rarely a good deal for my driving habits."

David R.

Texas Resident

Follow the exact steps to get your result instantly and privately.

Drop in the car's sticker price (MSRP), what you plan to put down, and your local sales tax. Keep it realistic; this sets the baseline for both our lease and loan math.

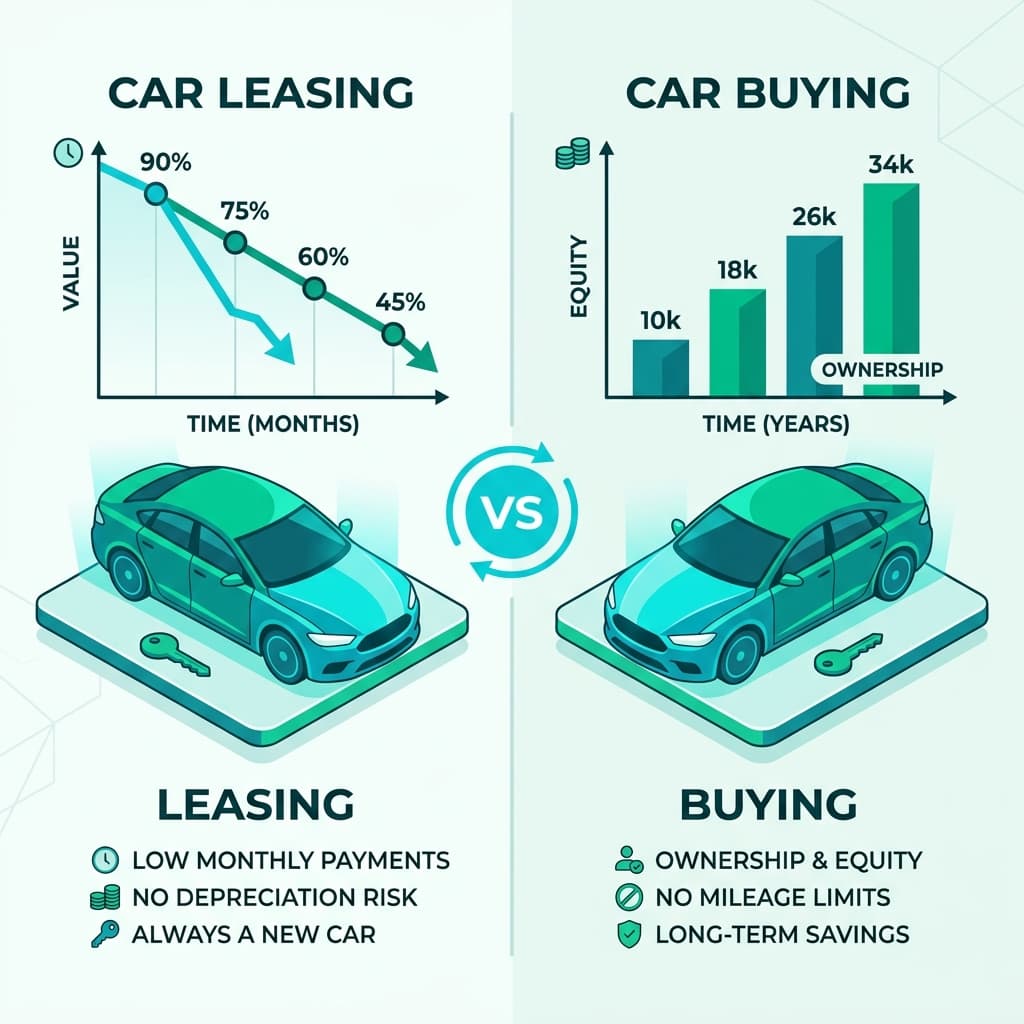

A lease payment is built on two simple pillars: depreciation and finance charges. The depreciation covers exactly what the car loses in value while it sits in your driveway (Cap Cost minus [Residual Value](/blog/residual-value-car-lease-explained), spread over the term). The finance charge is the dealership's profit, driven by the [money factor](/blog/money-factor-explained). It looks tiny, but if you multiply it by 2,400, it reveals the brutal APR hiding underneath. Buying, on the other hand, is standard loan amortization. The monthly hit is harder because you are buying the whole car, not just renting it. But here is the critical difference: at the end of a loan, you own a massive asset. You can sell it, trade it, or drive it payment-free for years. That resale value is exactly why a loan with a painful monthly payment can still beat a cheap lease in the long run.

Every auto financing contract comes down to manipulating two variables: the rate of depreciation and the cost of borrowing money. Leasing makes you pay only for the slice of the car's life you use, while financing forces you to pay for the entire vehicle upfront. While leasing often boasts a smaller monthly footprint, it sacrifices equity. Ultimately, leasing is a long-term rental agreement that mathematically guarantees you will always have a car payment.

Lease Payment = [(Cap Cost − Residual) ÷ Term] + [(Cap Cost + Residual) × Money Factor]

Buy Payment = P × [r(1+r)ⁿ] ÷ [(1+r)ⁿ − 1]Let's look at a $35,000 car with $2,000 down. On a 36-month lease with a 55% residual and a 0.00125 money factor, you are looking at roughly $499 a month. Total out of pocket? $20,905—with zero equity to show for it. Buy that same car on a 60-month loan at 6.5% APR, and you are sweating a $694 monthly payment. But after 60 months, the loan dies. You subtract the estimated $15,530 resale value, bringing your net cost down to roughly $28,088. So, over the exact same period, the lease keeps about $7,180 more in your pocket today, but the loan leaves you owning a $15,500 asset tomorrow.

Auto Finance Content Reviewers

Our team breaks down the brutal reality of auto finance. We run the exact same mathematical formulas used by dealerships, stripping away the sales pitch so you can compare your leasing and buying options with absolute confidence.

Not every car leases equally well. These are the best cars to lease in 2026 based on residual value, manufacturer incentives, and real depreciation math.

Should you lease or buy your next car? This complete guide covers how both options work, the exact math behind each, who wins in which scenario, and every number to verify before you sign.

EV depreciation is brutal, federal tax credits favor leases, and automakers are inflating residuals. Here is the complete math on why leasing an electric car beats buying in 2026.

Here is the reality: Leasing almost always wins the monthly payment battle, but buying usually dominates the long game because you keep the car's resale equity. If you are wondering whether you should buy or lease a car, the correct choice depends entirely on your loan APR, the lease's [money factor](/blog/money-factor-explained), the [residual value](/blog/residual-value-car-lease-explained), and whether you hold cars for a decade. Run your numbers in our vehicle lease vs purchase calculator above to see the cold, hard truth.

The [money factor](/blog/money-factor-explained) is just the dealership's interest rate wearing a disguise. It looks like a harmless decimal (e.g., 0.00125), which dictates the finance charge on your lease. To unmask it into a normal APR, multiply that number by 2,400. In this case, 0.00125 is actually a 3% APR.

Think of [residual value](/blog/residual-value-car-lease-explained) as the car's projected worth when you hand the keys back. A high residual means the car holds its value well, which means you pay for less depreciation during your lease. Simply put: high residual equals a cheaper monthly payment. Every single time.

You have a few options. You can hand the car back, pay the disposition fee, and settle up for any [mileage overages](/blog/lease-mileage-limits-overage-charges) or damage. Or, you can execute a [lease buyout](/blog/lease-buyout-vs-return) and purchase the car for its set residual value. Just remember, if you walk away, you leave with zero equity.

Probably not. Leases come with strict annual mileage caps. Exceeding them triggers overage fees of roughly 15 to 30 cents per mile. If you commute heavily or take road trips, buying is the safer financial bet since racking up miles won't trigger massive penalty checks.

An acquisition fee is a mandatory upfront charge the leasing company slaps on to originate the lease (usually $595 to $995). Dealerships love to quietly roll this into your capitalized cost. We factor this directly into our calculator so nothing is hidden.

When you return your leased vehicle, the dealer charges you $300 to $400 to cover cleaning and prepping it for resale. You can sometimes dodge this fee if you immediately lease or buy another car from the same brand.

No. The leasing company's bank sets the residual value in stone. But you absolutely *can* [negotiate the capitalized cost](/blog/how-to-negotiate-a-car-lease) (the sale price of the vehicle) and sometimes the money factor. Haggling the sale price down is your best weapon for a cheaper lease.

Absolutely not. It lowers your monthly payment, but if you total the car pulling off the lot, that down payment instantly vanishes. It is vastly safer to roll the cost into the lease and negotiate the core price of the vehicle down instead.

Simple math: take the money factor and multiply it by 2,400. A dealer offering 0.00250 is secretly charging you about a 6% APR. Use this trick to compare lease financing directly against your pre-approved bank loans.

Yes, the core mathematical formulas for auto financing are universally applicable. Whether you need a car lease vs buy calculator UK, Canada, Australia, or India, you can use this tool. However, you will need to manually adjust the sales tax field to accurately reflect your local GST, VAT, or provincial taxes. Remember that terminology might differ slightly (for example, money factor is uniquely American; in other regions, you may just be given a straight APR to input).

You certainly can build one, but it is notoriously easy to break the formulas. The biggest trap with an Excel setup is miscalculating the conversion between a lease's money factor and a standard APR, or forgetting to amortize the loan properly. We built this tool so you do not have to write complex formulas in Excel—and we break down exactly why in our [Excel versus online calculator guide](/blog/excel-vs-online-calculator).

The current market in 2026 is defined by elevated loan APRs and volatile residual values, particularly with EVs. The biggest factors you must consider right now are: the dealership's markup on the money factor, the specific residual value assigned to your model, and any heavy manufacturer subsidies (lease cash). We break these down entirely in our guide on [factors to consider in 2026](/blog/factors-to-consider-2026).

No, we are not your financial planners. This tool provides incredibly accurate estimates based on standard industry math, but it cannot account for your specific state taxes, credit score variations, or local dealership fees. Always verify the final contract numbers before you sign.

While this is primarily an auto lease vs buy calculator, you can simulate a lease buyout by comparing your lease's end-of-term residual value against a used car loan. If you are looking for a lease calculator with trade in capabilities, simply subtract your positive trade-in equity from the negotiated capitalized cost or the loan amount before entering it into our tool. We also cover [lease with option to buy vs buy payment calculator](/blog/lease-buyout-vs-return) strategies in our guides.

The average car lease vs buy costs depend heavily on the residual value and money factor. As a rough estimate with current rates, a $35k car might lease for $400-$500/month, a $45k car for $550-$700/month, and a lease on a $50k car typically falls between $650-$850/month. For exact numbers, plug the MSRP into our total cost of buying a car calculator above.